How I Survived a Debt Crisis Without Losing My Mind

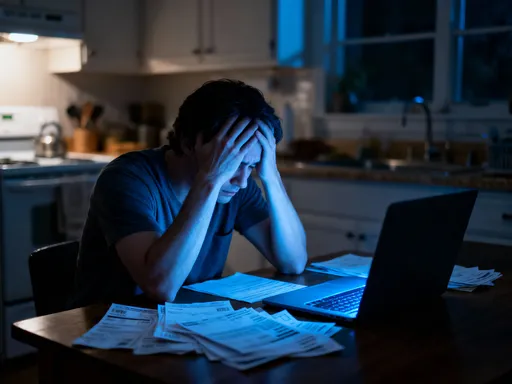

I once stood in my kitchen at 2 a.m., staring at a pile of bills, heart racing, wondering how I’d end up here. The debt kept growing, the stress kept rising, and I felt trapped. But I found a way out—not through luck, but through real, tested fund management strategies. This is how I took control, what actually worked, and how you can rebuild even when everything feels broken. It wasn’t a single decision that changed things, but a series of small, deliberate choices grounded in clarity, discipline, and self-compassion. The journey from crisis to stability is not linear, but it is possible. And it begins not with a windfall or miracle, but with a clear-eyed look at the numbers and a commitment to change.

Hitting Rock Bottom: The Moment I Realized I Was in a Crisis

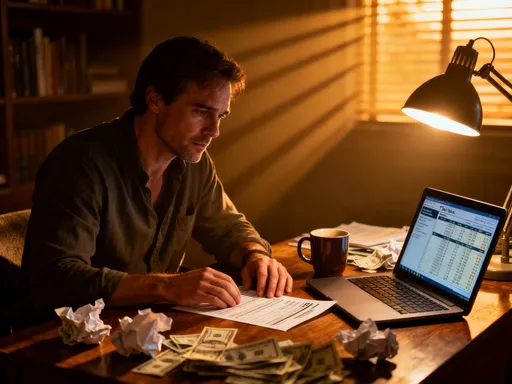

There is a moment—quiet, unannounced—when financial stress shifts from background noise to a full-body experience. For me, it came on a Tuesday night, though it could have been any night. I sat on the kitchen floor, a stack of envelopes spread around me like evidence of a crime I didn’t mean to commit. Credit card statements, overdue notices, utility disconnection warnings—all marked with red ink and final dates. My hands trembled as I added up the totals for the first time in over a year. The number was higher than I imagined: nearly $42,000 in unsecured debt, not counting my mortgage. I had been making minimum payments, convincing myself I was staying afloat, but in truth, I was sinking.

The emotional toll was just as heavy as the financial one. I felt shame, not because I had made reckless choices, but because I had stopped trying to understand them. I avoided opening mail. I ignored calls from creditors. I told myself things would get better next month, when the bonus came, or when the kids were older, or when life slowed down. But life never slows down. The bills do not wait. And denial, I learned, is not a strategy—it’s a delay of suffering. That night, I stopped pretending. I admitted I was in over my head. That admission was painful, but it was also freeing. It marked the end of avoidance and the beginning of action. Without that moment of surrender, no progress would have been possible. Hitting rock bottom isn’t a failure; it’s often the first honest step toward recovery.

Facing the Numbers: Why Hiding From Debt Makes It Worse

One of the most counterintuitive truths about debt is this: the more you avoid it, the more power it gains. When I finally decided to face my financial reality, I began by gathering every piece of paper that had anything to do with money. Credit card statements, loan agreements, bank statements, medical bills—everything. I spread them across the dining table and started listing each debt: the creditor, the balance, the interest rate, the minimum payment, and the due date. At first, the process felt overwhelming. Seeing all the numbers in one place was like standing in the middle of a storm. But as the list took shape, something unexpected happened: clarity replaced chaos.

Knowledge, even when uncomfortable, is power. By organizing my debts, I transformed them from vague sources of anxiety into specific, manageable problems. I could see exactly how much I owed, to whom, and at what cost. More importantly, I could calculate how long it would take to pay them off if I continued making only minimum payments—some estimates stretched beyond 15 years, with tens of thousands of dollars in interest. That realization was a wake-up call. I understood then that my old approach wasn’t just slow; it was financially destructive. Hiding from the numbers had only deepened the hole. Facing them, though painful, gave me the foundation to build a way out. Transparency didn’t solve my debt, but it made a solution possible.

This step is critical for anyone struggling with debt. You cannot manage what you do not measure. Avoiding your balances might provide temporary relief, but it prolongs the crisis. The act of recording your debts is not an invitation to panic—it’s an act of courage. It says, “I see you. I acknowledge you. And now, I will deal with you.” This is not financial advice from a distant expert; it’s a firsthand lesson from someone who lived in denial and paid the price. The first move toward freedom is simply to look at the truth, no matter how hard it is to face.

The Fund Management Shift: Treating Money Like a Tool, Not a Treat

For years, I treated money like a reward. When I had extra, I spent it—on dinners out, on clothes, on gifts. When money was tight, I tightened my belt temporarily, only to relax again when the next paycheck arrived. This cycle of feast and famine kept me reactive, never in control. The turning point came when I began to see money not as something to be spent, but as a tool to be managed. This shift in mindset changed everything. Instead of asking, “What can I afford this week?” I started asking, “What do I need to accomplish with my money this month?”

The core of this new approach was a simple cash flow system. I started by listing all my income sources—my salary, my spouse’s income, and any side earnings. Then, I categorized my expenses into three groups: essentials (rent, utilities, groceries, insurance), debt payments, and discretionary spending. For the first time, I created a monthly budget that assigned every dollar a job. This wasn’t about deprivation; it was about intention. I wasn’t cutting out joy—I was redirecting resources toward stability. One of the most powerful changes was redefining “paying yourself first.” Traditionally, that phrase means saving for retirement or building an emergency fund. But when you’re drowning in debt, the most important person to pay is yourself in the form of debt elimination. Every extra dollar I could free up went toward my highest-priority debt. That payment wasn’t just reducing a balance—it was restoring my sense of agency.

This system required discipline, but it also brought peace. I no longer felt guilty about spending because I knew my priorities were covered. I could still enjoy a movie night or a small gift for a grandchild, but only after the essentials and debt payments were accounted for. Money became predictable, less of a source of stress and more of a partner in my recovery. The emotional benefit was just as important as the financial one. I began to trust myself again. I was no longer at the mercy of impulses or unexpected bills. I had a plan, and that plan gave me back a sense of control I hadn’t realized I’d lost.

The Debt Avalanche vs. Snowball Debate: Which Really Works?

Once I had a clear picture of my debts and a budget in place, the next question was: where to start? Two popular methods emerged in my research: the debt avalanche and the debt snowball. The avalanche method prioritizes debts with the highest interest rates first, minimizing the total interest paid over time. Mathematically, it’s the most efficient. The snowball method, on the other hand, focuses on paying off the smallest balances first, regardless of interest rate. Psychologically, it builds momentum by delivering quick wins. Both have merit, but the right choice depends on your personality, motivation style, and level of financial discipline.

I initially leaned toward the avalanche method. It made logical sense—I wanted to save as much money as possible. I started attacking my highest-interest credit card, which carried a 24.99% APR. I threw every extra dollar at it while making minimum payments on the others. After four months, I paid it off. The relief was real, but so was the frustration. The balance had been large, and progress felt slow. Meanwhile, my smaller medical bill—only $1,200—was still there, a constant reminder of how much I owed. I realized I needed more frequent wins to stay motivated. So, I switched to a hybrid approach. I kept the avalanche method for my largest, highest-interest debts, but I used the snowball method for smaller balances. This allowed me to maintain long-term efficiency while also feeding my need for progress.

The truth is, no single method fits everyone. If you’re highly analytical and patient, the avalanche may work better. If you thrive on encouragement and visible results, the snowball could keep you going. What matters most is consistency. The best repayment strategy is the one you can stick to. Some experts argue passionately for one method over the other, but in practice, flexibility often leads to greater success. I found that combining logic with emotional intelligence made the journey sustainable. I saved money on interest while also celebrating small victories. Both are important. Debt repayment isn’t just a math problem—it’s a human experience. The method you choose should serve both your wallet and your mindset.

Cutting Costs Without Killing Joy: Smart Trade-Offs That Stick

When people think about getting out of debt, they often imagine extreme sacrifice: no dining out, no vacations, no gifts, no pleasures at all. But that kind of deprivation rarely lasts. I learned that the key to sustainable cost reduction isn’t cutting everything you love—it’s making thoughtful trade-offs that free up money without making you feel punished. The goal isn’t to live poorly; it’s to live intentionally. I began by reviewing my monthly spending and asking one question for each expense: “Does this add real value to my life?” Some things passed the test easily—my internet bill, for example, allowed me to work from home and stay connected with family. Others didn’t—like the three streaming services I barely used.

I canceled two of them and kept only the one with the shows I actually watched. That saved $28 a month—small, but meaningful. I renegotiated my cell phone plan by switching to a family discount program, cutting another $35 per month. I started buying groceries with a list and avoided shopping when hungry, which reduced impulse buys. I switched to generic brands for household items and medications, saving about $100 a month. I stopped using credit cards for daily purchases and switched to cash or debit, which made me more aware of spending. These changes weren’t dramatic, but they added up. Within three months, I had redirected over $300 a month toward debt payments—money I hadn’t known I could free up.

Importantly, I didn’t eliminate joy. I still hosted birthday dinners, but I did them at home instead of at restaurants. I still bought gifts, but I focused on thoughtful, handmade ones. I found that these choices often brought more meaning than the expensive alternatives. Cutting costs became less about loss and more about prioritization. I protected the things that truly mattered—family, connection, peace of mind—while letting go of habits that drained my wallet without enriching my life. This approach was sustainable because it respected my dignity and emotional needs. Lasting change doesn’t come from punishment; it comes from balance.

Building a Buffer: Why Emergency Funds Matter Even in Debt

One of the most controversial pieces of advice I encountered was this: start saving a small emergency fund even while paying off debt. At first, it made no sense. How could I save money when I owed so much? Wouldn’t that slow down my progress? But then I experienced a flat tire—$450 at the mechanic. I didn’t have the cash, so I put it on a credit card. That single event added to my debt and erased two months of hard work. I realized then that without a buffer, any unexpected expense could trigger a setback. That’s when I started building a mini emergency fund—just $500 at first, then $1,000. I treated it like a non-negotiable expense, just like rent or a debt payment.

This fund wasn’t meant for vacations or shopping—it was a safety net for true emergencies: car repairs, medical copays, appliance breakdowns. Having it changed my relationship with stress. When my washing machine stopped working, I paid for repairs without panic or new debt. That $500 protected thousands in progress. Financial experts often debate whether to save or pay off debt first, but the reality is that both are necessary. Without debt repayment, you’re sinking. Without savings, you’re vulnerable. The two goals aren’t opposites—they’re partners in stability. I found that even a small fund reduced anxiety and increased confidence. It signaled that I was no longer living paycheck to paycheck, even if I still had balances to clear.

Building this buffer required discipline, but it paid off quickly. I started with $20 a week—less than the cost of a weekly coffee run. Over time, it grew. I protected it by not dipping into it for non-emergencies. If I needed to use it, I prioritized replenishing it. This fund didn’t eliminate problems, but it prevented them from becoming disasters. It was a quiet but powerful form of self-respect: I was no longer willing to risk my progress for the sake of a few extra dollars toward debt. True financial health includes both forward motion and protection. One without the other is incomplete.

Staying on Track: Systems Over Willpower

Motivation fades. Willpower runs out. Emotions fluctuate. If your debt repayment plan relies on any of these, it will eventually fail. What doesn’t fail is a system. I learned this the hard way. There were months when I felt great—confident, focused, in control. Then came months of fatigue, family stress, or unexpected expenses. During those times, my old habits whispered: “Skip a payment. Just this once. You’ll catch up later.” But I had built systems that didn’t depend on how I felt. I set up automatic transfers to my debt accounts on payday. I scheduled monthly check-ins with myself to review progress and adjust the budget. I used a simple spreadsheet to track every payment and remaining balance. These tools kept me on course even when my energy was low.

Accountability also played a role. I didn’t share my journey with everyone, but I did confide in one trusted friend who was also working on her finances. We checked in every few weeks, not to compare numbers, but to encourage each other. That small connection made a difference. It reminded me I wasn’t alone. Systems don’t have to be complex. The most effective ones are simple, repeatable, and automatic. They remove the need for daily decisions. You don’t have to muster willpower to pay a bill that’s already scheduled. You don’t have to debate spending when your budget is already set. Over time, these habits became second nature. The work didn’t get easier, but it got smoother. I stopped seeing debt repayment as a battle and started seeing it as a practice—one that improved with consistency, not perfection.

This shift in perspective was crucial. I stopped waiting to feel ready or inspired. I showed up anyway. I followed the system, even on hard days. And that, more than any single payment, was what brought lasting change. Discipline isn’t the absence of struggle; it’s the presence of structure. When emotions run high, systems keep you grounded. They turn intention into action, day after day, until the outcome is no longer in doubt.

From Crisis to Control—What I Learned for Good

Today, I am not debt-free, but I am in control. That distinction matters. Freedom from debt isn’t just about the numbers; it’s about the mindset. I no longer feel trapped. I know how to manage my money, how to respond to setbacks, and how to stay on track without losing myself. The journey taught me that financial recovery isn’t a sprint or even a marathon—it’s a series of small, repeated choices. It’s not about perfection. It’s about persistence. It’s about getting back up when you slip, adjusting when life changes, and continuing forward even when progress feels slow.

The strategies that helped me—facing the numbers, creating a budget, choosing a repayment method, cutting costs wisely, building a buffer, and relying on systems—are not magic. They are practical, accessible, and within reach for anyone willing to try. They don’t require a higher income or a financial degree. They require honesty, effort, and time. But they work. More than that, they transform the way you see yourself. You stop being a victim of circumstance and start being the author of your financial story. That shift is the real victory. Debt can feel overwhelming, but it is not unbeatable. With better fund management, clear goals, and consistent action, what once seemed impossible becomes not just possible, but empowering. The road out of debt is not easy, but it is worth every step.